%20(1640%20x%20650%20px)%20(1640%20x%20500%20px).png)

How the War on Iran Could Make Maharani Freeport Asia’s Next Oil Hub

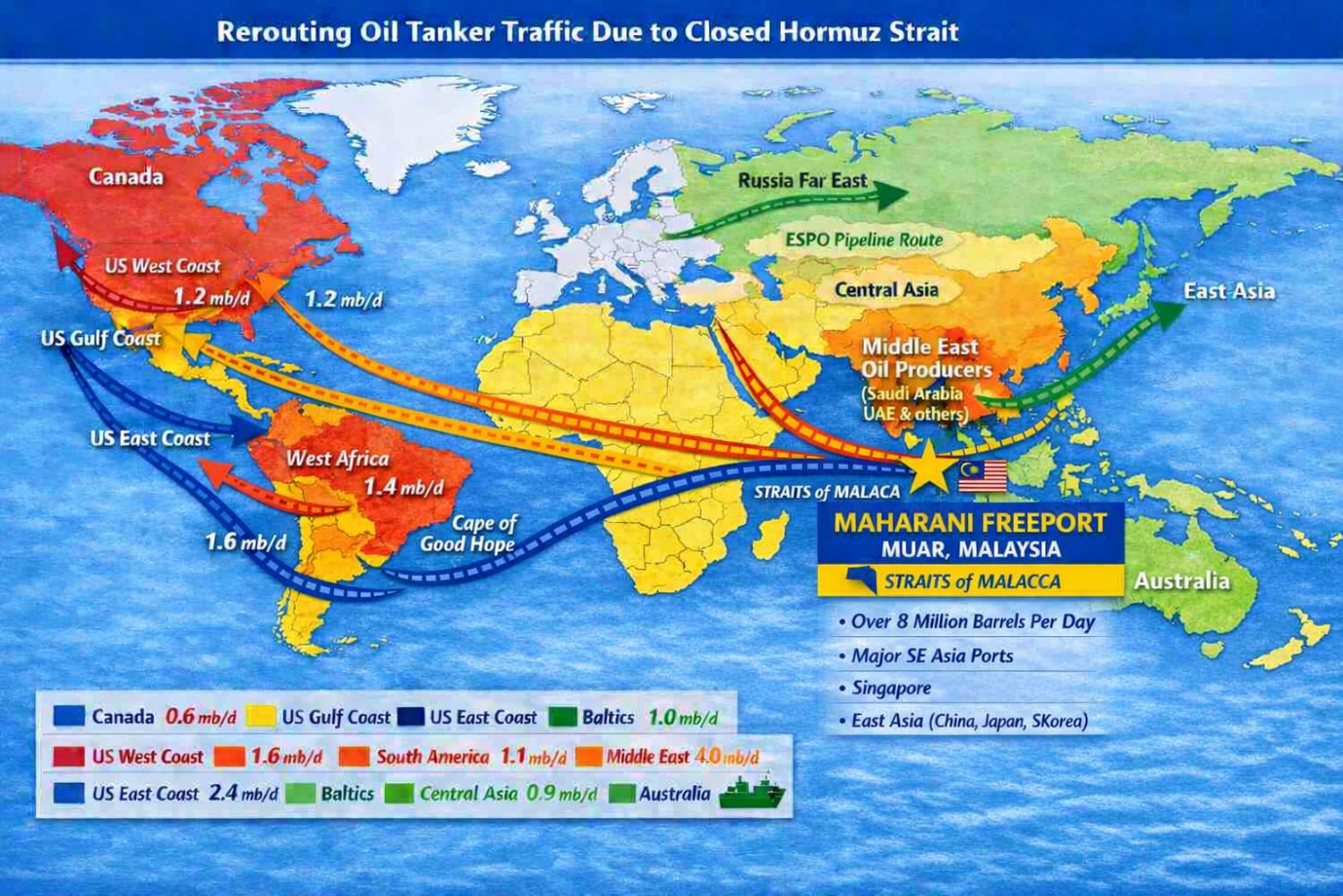

I. The Hormuz Shock and Malacca Strait Opportunity

The protracted US-Israel war on Iran has done what analysts warned it would: throttled the Strait of Hormuz and thrown 20% of global oil supply into jeopardy. Freight rates and war-risk insurance premiums have surged.

Importers across China, Japan, South Korea, India and Southeast Asia — long reliant on just-in-time Gulf deliveries — are scrambling for buffer storage closer to home. Almost half of Malaysia's oil supply transits via the Hormuz waterway.

Into this dislocation steps Maharani Freeport, a deepwater energy complex in the river town of Muar, Johor, engineered to catapult a quiet backwater into Malaysia's next major port city, targeting RM144 billion (US$35.8 billion) in long-term investments and to generate over 45,000 jobs.

Launched in November 2025 as the country's first duty-exempt energy freeport, it can berth Very Large Crude Carriers (VLCCs), blend oil products, conduct ship-to-ship (STS) transfers, and function as a full logistics and trading hub for redistribution across Asia.

The broader neighbourhood is already critical infrastructure. Some 100,000 vessels transit the Malacca Strait annually, carrying a quarter of global seaborne oil.

Maharani sits within a cluster of established energy terminals: Petronas' Melaka Energy Park, Pengerang Integrated Petroleum Complex, and Tanjung Bin Energy Hub. Together with Singapore and Indonesia's Riau Islands, these ports form a natural regional oil buffer — reserve banks of crude and products that can be mobilised when the Middle East bleeds supply.

Other than Malaysia's own production of premium light sweet crudes, which are largely exported, and other Asia-Pacific grades, alternative supply sources and sea routes include Russia, via two key corridors. The ESPO Pipeline linking Kozmino port on the Russian Pacific coast provides an eastward sea route to Southeast Asia, bypassing all Middle East chokepoints. And the Baltic/Black Sea route around the Cape of Good Hope to the Indian Ocean and then the Malacca Strait is longer, but viable.

The ESPO corridor is currently the most operationally clean route for South East Asia: no hostile straits, shorter voyage to Malaysia than Atlantic alternatives, and with the US sanctions waiver in place, it is politically accessible for now.

Russia currently produces around 9.87 million barrels/day, with China increasing overland pipeline imports from Russia and Kazakhstan, creating a parallel supply chain bypassing traditional Western-influenced energy flows.

Asia is also importing record volumes of fuel oil — used by ships and utilities — from Russia in March 2026, after the US government eased sanctions to reduce pressure on international oil markets, with Singapore and Malaysia among the top recipients.

Another long but stable supply route is from the United States, which produced 13.58 million barrels/day last year, making it the world's largest oil producer. US West Texas Intermediate and Eagle Ford grades travel the Pacific route via the US Gulf Coast, Panama Canal, the Pacific Ocean and the Malacca Strait. Supply from the US West Coast (California) travels directly via the transpacific route to South East Asia.

Analysts caution that crude from the US, South America, or West Africa is too distant for immediate relief, as shipments won't arrive for months. However, for medium-term planning they are strategically sound.

These include crude from Brazil's Lula and Búzios fields, which transits the Atlantic coast, via the Cape of Good Hope to the Indian Ocean, or via Cape Horn on the Pacific route. Supply from West Africa — Nigeria, Angola, Gabon — is well-suited to Asian refineries and has long been a significant alternative supplier, journeying around the Cape of Good Hope, via the Indian Ocean to South East Asia.

From Central Asia, crude from Kazakhstan and Azerbaijan moves via China's pipeline corridor. While landlocked, Kazakhstan's crude reaches Asia via the CPC pipeline, the Black Sea, moving by tanker to the Cape of Good Hope, and the Kazakhstan-China pipeline provides overland delivery and is relevant if transiting or re-exporting through China to South East Asian markets.

Crisis accompanied Maharani's opening. When prices swung toward $110/barrel, traders store oil and hunt profitable spreads. Tank farms and blending terminals fill up. Cargo routes get redesigned around safe middle-point hubs — Singapore and the Riau Islands, Fujairah in the UAE, Zhoushan in China. The UAE's Fujairah built its global relevance this way: growing from a minor Gulf outpost into a major storage hub through successive waves of Gulf tensions from the 1980s through the early 2000s. Maharani now has the same structural opening.

II. The SEZ Edge: Singapore Trades, Johor Stores

The Johor-Singapore Special Economic Zone (SEZ) is the institutional scaffold that gives Maharani its competitive logic. Singapore brings what Johor cannot easily replicate: established commodity trading houses, deep financing markets, a functioning derivatives and pricing exchange, maritime law and arbitration, and the Global Trader Programme — Enterprise Singapore's tax incentive scheme that has lured some of the world's top oil traders to set up desks in the city-state.

Johor brings what Singapore has run out of: land.

The division of labour is clean. A trader based in Singapore buys Middle Eastern crude via a Singapore-licensed entity, finances it through a Singapore bank, hedges it on the Singapore Exchange — then stores it just across the causeway in Johor at a fraction of the cost. The trading ecosystem stays intact; the physical oil doesn't have to.

This reflects established corridors in the West. The Amsterdam-Rotterdam-Antwerp (ARA) triangle combines Europe's premier financial trading centres with its largest port and refining complex. The Houston-Louisiana corridor does the same for the United States. The Johor-Singapore corridor is Asia's answer to both — and Maharani Freeport, positioned north of the main industrial zone along the Malacca shipping lane, is the missing node: a storage hub, blending centre, bunkering station and transshipment point that the corridor needs to function at full capacity.

Singapore's physical storage market is visibly strained. Onshore capacity — concentrated on Jurong Island and Pulau Bukom — is constrained by land scarcity and rising sea levels that require terminal operators to fund their own sea walls. When tanks brim up, traders anchor supertankers offshore as floating storage: that count has exceeded 60 vessels at peak versus a normal 30–40, congesting the Singapore Strait and raising collision and spill risks.

Johor and Indonesia's Riau Islands are the pressure valve. S&P Global Platts recognised this reality when it broadened its benchmark methodology in 2015 from Singapore-only to a "FOB Straits" system encompassing terminals in both countries.

The Johor terminals already embedded in the Platts pricing window include Tanjung Langsat (part of the Tanjung Langsat Industrial Complex, with extensive petroleum and chemical storage), Tanjung Bin (over 1.4 million cubic metres of capacity, operated by a Vitol-MISC joint venture, VLCC-capable), and Pengerang Integrated Complex (over 5 million cubic metres, operated by Dialog Group, integrated with Petronas' RAPID refinery).

In Riau Islands, Kabil Terminal in Batam and Tanjung Uban in Bintan are approved delivery points for fuel oil and middle distillates.

III. The Platts Test: Benchmark or Backwater?

Here is where Maharani Freeport's long-term fate will be decided — not in a war room, but in a pricing window. If cargoes traded at Maharani become deliverable in Platts' Market on Close (MOC) process, they enter the methodology that sets the Mean of Platts Singapore (MOPS) benchmark — the reference price for oil trade across Asia. That is the gateway to becoming a real, permanent trading hub rather than a crisis-era overflow depot.

Platts' criteria are exacting. To be included in the FOB Straits pricing window, a terminal must demonstrate: sufficient tankage, blending and VLCC-sized loading infrastructure; transparent, open reporting of cargo movements accessible to third parties, not just a single-anchor company; active, multi-party trading — not just storage leases — with credible counterparties willing to both deliver and lift cargoes; and full alignment with regional customs, tax and regulatory frameworks so cargoes can be freely traded without restriction.

Maharani has approached S&P Global Platts for inclusion in the process, and discussions between the two parties have been taking place since February, an official with Maharani Energy Gateway (MEG) said.

Maharani needs to pass that threshold. As of now, no publicly confirmed cargo trades involving named global trading houses have been reported — the port is still in early ramp-up mode. Any transactions that took place are largely via ship-to-ship transfers involving smaller parties, while no major traders were heard to have taken up long-term storage leases yet.

These include neighbouring countries seeking storage space for oil stocks, the official added.

According to shipping agents, there had been no active vessel calls yet at the port, where activities are mainly for STS and layup, and ships spending time on matters such as change of ownership, or when a vessel has a few days of downtime.

Inclusion in the Platts MOC process demands a credible roster of global participants including Vitol, Trafigura, Shell, Glencore — the names that move benchmark markets. Maharani Energy Gateway will need to attract them, not merely accommodate them, and persuade them to take up long-term storage leases like those made in Singapore.

It will also need to develop differentiated services — sour condensate blending, green hydrogen and green ammonia production (for which MEG has already pursued CCGT power plant and green fuel partnerships), and long-term storage contracts with major players such as PetroChina — to lock in volumes beyond the crisis cycle.

One major green project in Maharani Freeport is a liquefied biomethane plant. This was signed in December 2025 between China Petroleum Global Guangdong Co. (via China Huanqiu Corp.) and Singapore's Straits Bio-LNG to convert biomass — palm oil waste — into biomethane and then liquefied biomethane.

The agreement covers the full EPC chain (engineering, procurement, construction, commissioning), and the plant will be developed in two phases. So far, on-site preparation is in progress, involving an assessment of soil settlement of the reclaimed sea areas on the island.

The company has targeted delivery to global markets around late 2027, helping to fill the supply gap for clean and renewable gas.

The history of commodity hubs is unforgiving: terminals that ride a crisis into relevance but fail to institutionalise that role slide back into obscurity the moment supply chains normalise.

Maharani Freeport has the location, the infrastructure mandate, and now the geopolitical tailwind. The question is whether it can convert a wartime surge into a peacetime franchise — by meeting Platts' criteria, attracting multi-party trading, and proving it can handle benchmark cargoes. The clock is ticking.

Hours before President Donald Trump's April 8 ultimatum expired, Washington and Tehran struck a two-week ceasefire. Under the deal, Iran agreed to temporarily reopen the Strait of Hormuz, restoring the flow of oil, gas, and fertilizer cargoes through the world's most critical energy corridor.

The fragile truce offers a brief reprieve for the bruised global economy — but if it holds, it could also blunt Maharani Freeport's emerging role as the region's emergency oil bank amid the crisis.

.svg)